How Can SMEs Use Grant Advance Funding to Overcome Gaps Between Grant Award and Project Start?

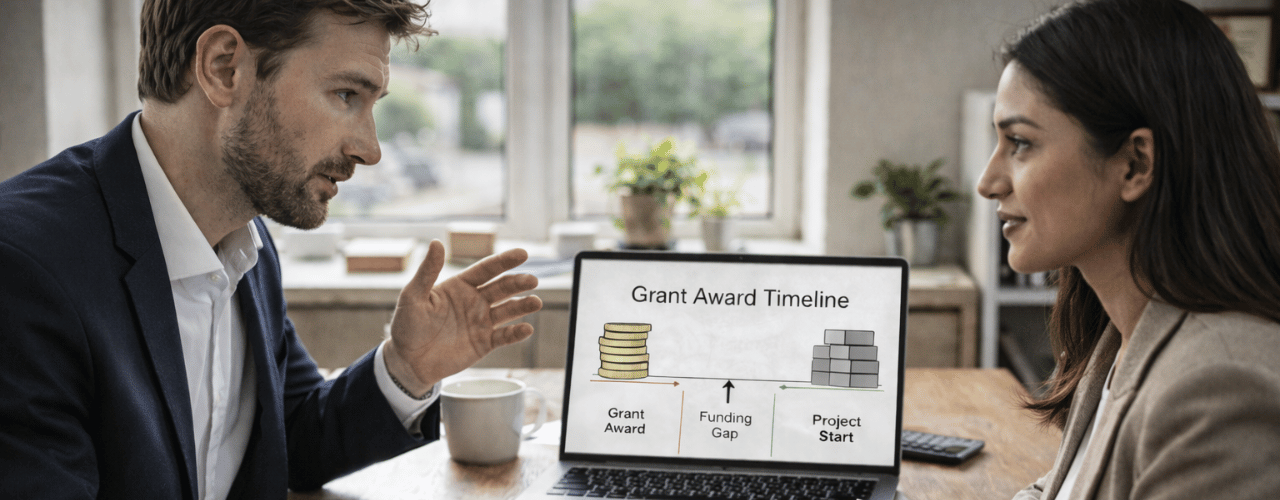

If you have secured an Innovate UK or similar innovation grant, you already understand one thing: the award letter does not fund next month’s payroll. Salaries fall due on fixed dates. Supplier deposits have payment terms. Delivery milestones do not move to match reimbursement timing. The funding gap between grant award and project start emerges at that point. Manage it early and mobilisation proceeds; leave it late and you compress runway.

Many Innovate UK and similar UK innovation grants operate on an arrears basis, with claims submitted for eligible costs incurred and paid. You incur eligible costs, compile evidence, submit the claim and the grant body reimburses you after review. You spend first and claim later. That structure does not change once the award is signed.

What Is a Funding Gap Between Grant Award and Project Start?

It is the period where you fund salaries, suppliers and project costs before the grant body releases the first milestone payment. Grant bodies release funds only after they validate evidence. When payroll runs monthly and reimbursement runs on review cycles, cash pressure appears quickly.

At the mobilisation stage, you need to know your exposure and your cash timeline. This is where structured Grant Advance Funding becomes practical. At SPRK, we structure funding against confirmed innovation awards so clients can mobilise before reimbursement lands.

Why Is There a Funding Gap Between Grant Award and Project Start?

Documentation quality, eligibility checks and administrative capacity inside the grant body determine payment timing. Even with a defined milestone schedule, reviewers extend the cycle when evidence requires clarification. Monitoring calls and follow-up questions can add further delay.

In practice, friction often comes from small breakdowns in evidence preparation. A supplier invoice coded incorrectly. Labour time not mapped cleanly to eligible activities. Cost categories that do not align precisely with the award letter. Each issue can shift reimbursement by weeks.

The sequence remains consistent:

- Agreement execution and confirmation of delivery dates

- Recruitment of specialist staff and engagement of contractors

- Placement of orders linked to milestone delivery

- Submission of evidence followed by review and validation

During that review window, burn rate continues. If reserves are tight, you slow recruitment or renegotiate supplier terms. Board conversations shift from growth to cash preservation.

What Costs Do SMEs Face Before the First Grant Payment Is Received?

Mobilisation compresses cash quickly. Early-stage expenditure typically includes:

- Specialist engineering salaries

- Contractor retainers secured upfront

- Equipment deposits and hardware procurement

- Software licences and cloud infrastructure

- Insurance, audit and compliance costs

Illustrative example: take a £300,000 grant with a 40 per cent funding rate (funding rates vary by competition and organisation size). If the first milestone requires £120,000 of eligible spend, you commit close to £80,000 before reimbursement. Two senior engineers at £5,000 to £6,000 per month each, plus employer costs, can exceed £15,000 monthly before contractor fees and overhead allocation. That exposure accumulates before the first claim passes review.

Delaying hires protects short-term liquidity but pushes delivery outward and risks moving milestones beyond their original forecast. In time-critical projects, delay can cost more than structured finance.

To manage that exposure, SPRK structures advance funding against confirmed grant awards so businesses can hire and commit to suppliers on schedule without altering ownership.

How Does Grant Advance Funding Work for Innovate UK Projects?

How does Grant Advance Funding work? You draw a portion of your confirmed grant before the grant body reimburses expenditure.

For Innovate UK projects, SPRK reviews your signed agreement, milestone structure and eligible cost profile. We focus on timing and delivery credibility, not the headline award amount. We assess whether cost categories align with the award and whether forecasts reflect realistic reimbursement timing.

In practice:

- You provide award documentation, cost breakdown and milestone schedule.

- We size the advance against upcoming expenditure using conservative projections.

- When the grant body releases the milestone payment, you repay the advance from those funds.

We assess runway, historic performance and delivery credibility. Clear reporting and precise cost mapping support faster decisions.

This moves you from waiting on reimbursement to funding delivery upfront, allowing you to maintain planned hiring and milestone schedules.

The advance must reflect realistic milestone timing. If your forecast assumes every claim clears at first submission, you introduce risk into the structure. First-time grant recipients can underestimate review lag in their initial cash model.

For more detail on how this structure works in practice, see our Innovation Grant Loans page. If you are participating in collaborative or sector-specific competitions, you can also review our guidance on Open Innovation Grant Programmes.

Can SMEs Combine Grant Advance Funding with Other Non-Dilutive Funding?

A single facility rarely addresses every liquidity pressure. Mobilisation, annual tax credit timing and scaling demands often overlap.

Using Advance Funding for Milestone Liquidity

Grant Advance Funding bridges defined milestone-related cash gaps and keeps delivery aligned with agreed timelines.

When an R&D Tax Credit Loan Adds Stability

An R&D tax credit loan accelerates access to expected HMRC refunds within the financial year. You do not wait until year-end submission and processing. That acceleration stabilises runway when grant reimbursement and tax credit timing intersect, giving clearer visibility over cash position.

Used alongside advance funding, it reduces dependence on overdrafts and avoids equity discussions driven purely by short-term timing gaps.

Learn more about how R&D Tax Credit Loans can support annual liquidity cycles.

When an Innovation Term Loan Extends Runway

Where delivery spans multiple milestones or hiring accelerates, an innovation term loan extends working capital across a longer horizon. Structured repayment allows clearer planning around recruitment and supplier commitments.

A disciplined funding structure may combine:

- Grant Advance Funding for mobilisation

- An R&D tax credit loan for annual claim acceleration

- An innovation term loan for extended runway stability

Each facility covers a different timing exposure.

Explore how Innovation Term Loans support scaling innovation-led businesses.

How Should SMEs Plan Cash Flow Around Innovate UK Grant Reimbursement Timelines?

Funding tools help, but cash modelling determines whether they work.

When you deliver an Innovate UK-funded project, build your forecast around evidence review cycles, monitoring calls and possible clarification delays. Assume friction and model conservatively.

Focus on:

- Conservative milestone reimbursement assumptions

- Weekly net cash tracking during mobilisation

- Stress testing 60 to 90-day reimbursement delays

- Hiring decisions tied to confirmed funding visibility

- Supplier contracts structured around realistic drawdown timing

Advance funding should sit inside that model. You need visibility over funding envelope, repayment dates and burn rate.

Many projects do not fail because funding is unavailable. They stall because timing was misjudged.

What Are the Grant Advance Funding Eligibility Criteria for SMEs?

Grant Advance Funding eligibility criteria typically include:

- A confirmed award and executed agreement

- Defined milestone structure

- Clearly identified eligible costs

- Sufficient visibility over delivery timelines

Conditional awards, incomplete documentation or unclear cost allocation weaken the case for advance funding. Lenders look for discipline and transparency.

You remain accountable for delivery and compliance. Advance funding supports execution; it does not transfer responsibility.

Why Does Closing the Funding Gap Early Strengthen Project Delivery?

Closing the funding gap stabilises mobilisation. You recruit when required, commit to suppliers with confidence and complete milestones on schedule.

When runway feels controlled, boards focus on delivery rather than short-term cash pressure.

SPRK works with UK innovation-led SMEs to structure non-dilutive funding aligned with delivery milestones, tax credit timing and growth plans. Combined with complementary tools such as an R&D tax credit loan or innovation term loan, Grant Advance Funding helps spread timing risk and maintain delivery momentum.

From Grant Award to Funded Mobilisation

An innovation grant confirms your project has funding approval for delivery. It does not remove timing risk.

The gap between award and reimbursement is structural. Anticipate it, model it and structure funding around it to protect delivery.

If mobilisation begins within the next 30 to 60 days, review milestone timing, cash runway and funding structure now. Early structuring generally provides more control than reactive financing under pressure.

If you have a confirmed grant award and a defined project start date, speak to SPRK before your first major cost lands. A short review of your milestone schedule, cash runway and funding options will clarify whether Grant Advance Funding, an R&D tax credit loan or a wider innovation term facility is appropriate. You can contact our team to discuss your project structure and timelines in confidence.